Market Response to India-Pakistan Ceasefire Impacts Defence Stocks

On a recent Monday trade, defence equities demonstrated a diverse market behavior following the consensus between India and Pakistan to establish a ceasefire. This agreement came in the wake of an intense escalation that lasted over 90 hours, instigated by Operation Sindoor, India’s response to the Pahalgam attack. Renowned firms such as Bharat Electronics and Bharat Dynamics indicated an upward trend in their stocks, each rising by approximately 1%, while Hindustan Aeronautics evidenced a slight slump, decreasing by just over 1%.

Conversely, shares of other defence companies like Zen Technologies, Unimech Aerospace, and Krishna Defence experienced an uptick of up to 5%. Meanwhile, the stocks of Paras Defence, Astra Microwave, and Apollo Micro Systems showed a downward trend and dropped up to 6%.

The Nifty Defence Index, introduced in November 2024, has eclipsed the performance of broader indices like the Nifty 50 and the Nifty Midcap 100 over the last month. The Defence Index has gained 18% compared to 8% for the Nifty and 9% for the Nifty Midcap since April 9, 2025.

The defence sector’s long-term economic stability derives from a strategic vision to prioritize local defence manufacturing, part of the Atmanirbhar Bharat campaign. A steady attention towards import replacement, a heightened allocation towards defence capex, and incorporating public-private partnerships are shaping a solid foundation.

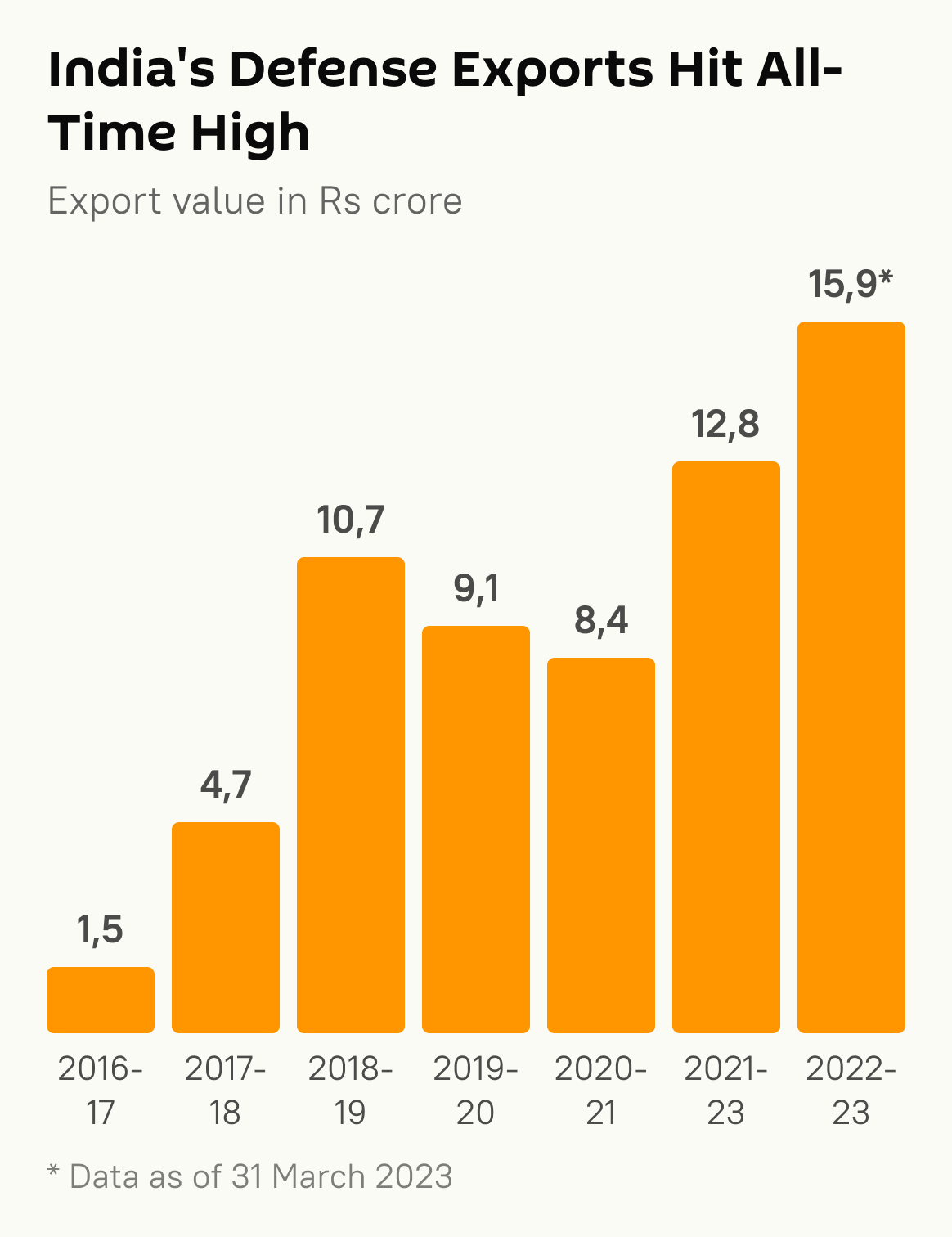

In the fiscal year 2025, India pledged over INR 6.2 lakh crore to defence, with an impressive allocation of INR 1.72 lakh crore dedicated solely to capital expenditure. This allotment is anticipated to grow further due to the current geopolitical climate.

Indigenous companies like BEL and HAL are significant beneficiaries of the Make in India for Defence initiative, acquiring significant domestic contracts for radar systems, helicopters, and avionic devices. Similarly, firms like HAL and BDL have displayed a growing tendency toward exports, concentrating particularly on Southeast Asian, African, and Latin American countries.

A noteworthy shift in the defence landscape is the increased participation from private sector contenders like L&T Defence, Data Patterns, and Bharat Forge, which have diligently expanded their defence portfolios, marking a significant shift from the traditional dominance of Public Sector Undertakings (PSUs).

Another vital aspect of the sector’s development is a high investment in technology and R&D. Thanks to the backing of DRDO programs and government support, companies are focusing more and more on developing indigenous platforms and advanced systems, thus enhancing future scalability. The robust order books of these firms are projected to further expand.

Operation Sindoor brings along an increased focus on the pace of execution within defence corporations. These firms are anticipated to face more aggressive execution targets, which are expected to become evident within a few quarters to 1-3 years, potentially leading to a surge in revenues and earnings forecast.

In parallel, companies operating in other sectors related to defence, like cybersecurity, strategic minerals & rare earths, oil & gas, hydro-projects, military EPC, military logistics and railways are also likely to witness expedited execution.

Notwithstanding this optimistic outlook, one must approach investment decisions with caution. Investments should be centered on enterprises that demonstrate attractive valuations and comply with the criteria of scientific investing.

From a fundamental and technical viewpoint, some stocks appear appealing. Hindustan Aeronautics Ltd (HAL), a premier player in the field of aircraft manufacturing, flaunts a sturdy order book, and its ongoing production of Tejas Mk1A. The joint venture it has with Safran for engine development further enhances the long-term potential of the firm.

Similarly, Bharat Dynamics Ltd (BDL), a principal producer of missile systems, has a strong pipeline. The company’s recent joint effort with MBDA (Europe) has further augmented its capacity. Another entity benefiting from India’s naval modernization events, Mazagon Dock Shipbuilders, is engaged in creating advanced submarines and stealth frigates under Project 75 and other agreements.

Paras Defence is another fascinating player in the sector, given its specialised contributions in optoelectronics, space optics, and defence electronics systems. The firm has established a niche in high-precision components and remains an integral part of India’s defence and space supply chains. It boasts a healthy order book, consistent revenue growth, and maintains strong client relationships with DRDO and ISRO.

Finally, looking at the wider picture – defence stocks are not merely event-driven entities but rather long-term investments. As India is set to become the world’s third-largest defence spender by 2026, the sector promises a 5–7-year growth trajectory. While events like Operation Sindoor’s aftermath may introduce market volatility, aligning with historical trends and policy suggest dips could be viewed as opportunities for purchase instead of sell signals. Even amidst turbulence, the markets prevail.