Software Stocks Snowflake and Okta Outperform in Tech Sector

Year to date, software stocks are significantly outshining their hardware counterparts in the tech sector, sporting a 26 percentage point advantage. In the current market landscape, software companies, especially those focusing on artificial intelligence (AI), possess a unique allure primarily due to their immunity to tariffs. Two such companies worth investor consideration are Snowflake and Okta.

These two companies have outperformed the larger software industry during the first five months of 2025, signaling a brighter future according to Wall Street analysts. They project further growth in the upcoming year. As of now, 50 analysts are closely monitoring Snowflake, estimating a median target price of $222 per share.

This estimation forecasts an 8% growth from the present share cost of $205. When we bring our attention to Okta, a similar story unfolds. From the 47 analysts tracking this company, they predict a median target price of $130 per share.

If these projections hold true, this would represent a 26% growth from the current $103 share price. Hence, if an investor has a budget of $450, splitting it equally across Snowflake and Okta could be a wise strategy.

Snowflake primarily focuses on data analytics and offers a powerful cloud platform that assists customers in unifying, understanding, and transforming data. The platform also supports data sharing and monetization, AI model creation, and the development of data-driven applications.

Technology consulting firm Gartner saw Snowflake’s potential and lauded the company as a leading force in the realm of database management systems. The past two years have witnessed Snowflake’s concentrated efforts towards augmenting its platform with a variety of AI capabilities.

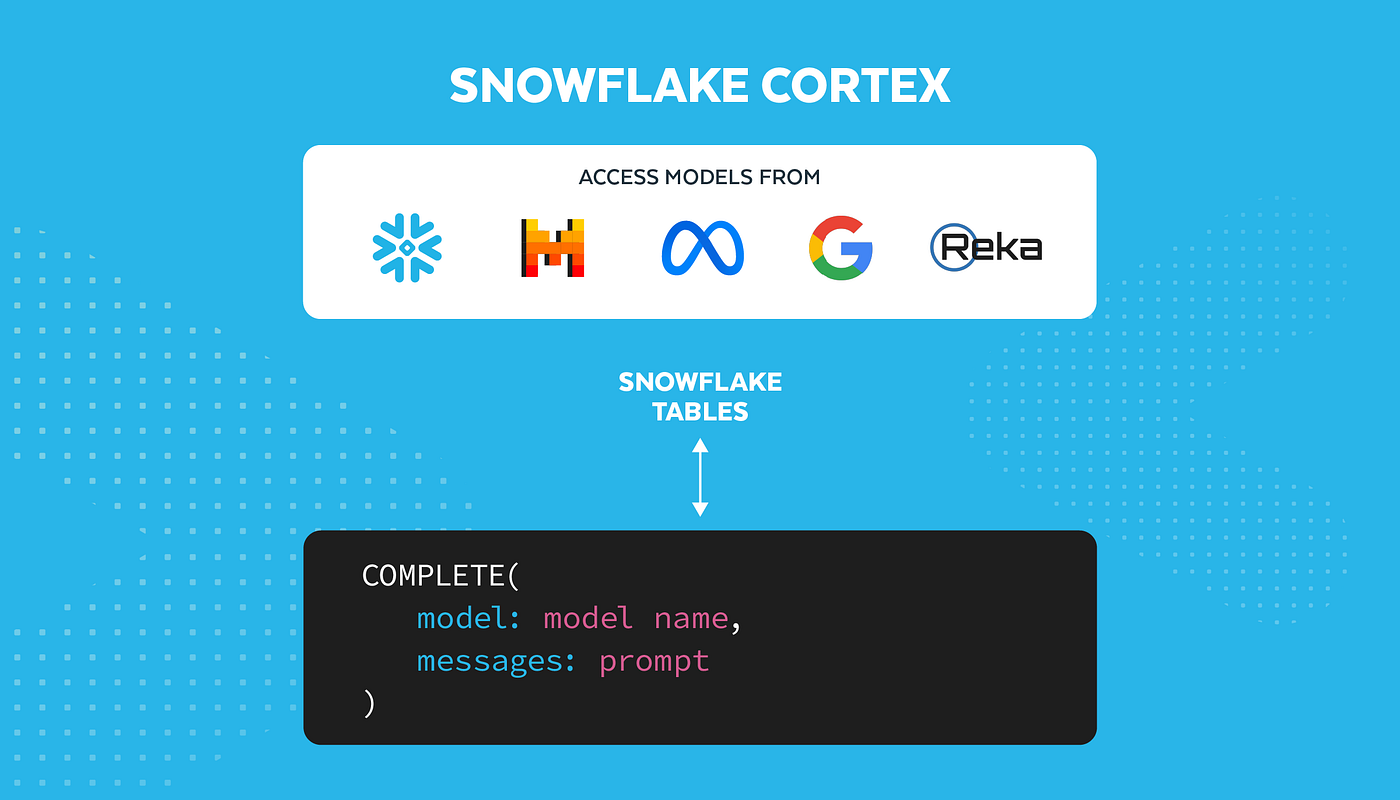

One notable feat is their Cortex AI, a fully managed service that includes a custom large language model called Arctic. Arctic serves to dissect information, summarize it, and respond to queries using natural language. In addition to this, Snowflake has also incorporated AI tools for anomaly detection, classification, and forecasting purposes.

Snowflake had a bright start to fiscal 2026 as the first quarter results, unveiled in April, surpassed expectations. The number of customers rose by 18% resultant in a total of 11,578 and the average spending by existing customers climbed by 24%. Following these positive results, revenue saw a significant increase of 26%, reaching $1 billion, with non-GAAP net income growing by a whopping 71% to $0.24 per diluted share.

This inspired the company to raise its full-year guidance, projecting a 25% increase in revenue. Looking towards the future, Snowflake’s total addressable market is predicted to reach $342 billion by 2028. According to analysts, Snowflake can expect its adjusted earnings to grow at an annual rate of 35% all the way through fiscal 2027. It’s worth noting that the company outperformed average consensus earnings estimates by 34% in the past six quarters.

Examining Okta, it specializes in Identity and Access Management (IAM) software contributing to enhancing cybersecurity. This system permits administrators to manage and assign system permissions, ensuring only intended users and devices can engage with applications and resources. Notably, Okta’s platform incorporates AI technology to authenticate users and continuously evaluate risk.

For eight years in a row, Gartner recognized Okta as a titan in the industry. Okta’s wide array of solutions tailors to both customer and workforce identity needs. They supplement their core IAM packages with Privileged Access Management (PAM) and Identity Governance and Administration (IGA) products.

PAM serves as the shield for highly sensitive superuser accounts while IGA streamlines compliance reporting and automates IAM processes. As of the first quarter of fiscal 2026, which concluded in April, Okta’s revenue climbed 12% to a total of $688 million, and non-GAAP net income saw a notable increase of 32% reaching $0.86 per diluted share.

In spite of these positive outcomes, Okta’s stock took a hit post-reporting as the management refrained from raising full-year guidance, pointing towards macroeconomic uncertainties. Nevertheless, Okta envisions its total addressable market to be $80 billion.

Wall Street projects that Okta’s earnings will grow at a 10% annual rate through fiscal 2027. During the last six quarters, Okta has been successful in surpassing consensus earnings estimates by an average rate of 15%. It’s anticipated that IAM spending will see an annual growth rate of 12.6% through 2030.

Presupposing Okta keeps up with the market’s pace, it is poised to exceed consensus earnings estimates. In light of this potentiality, it seems profitable for investors to take a small position in Okta at this time.

Summarizing, both Snowflake and Okta situate themselves as promising prospects in the software industry with immense growth potential. Through strategic investments in these companies, investors can exploit the current favorable position of software stocks in the tech sector, optimizing gains while contributing to their growth.