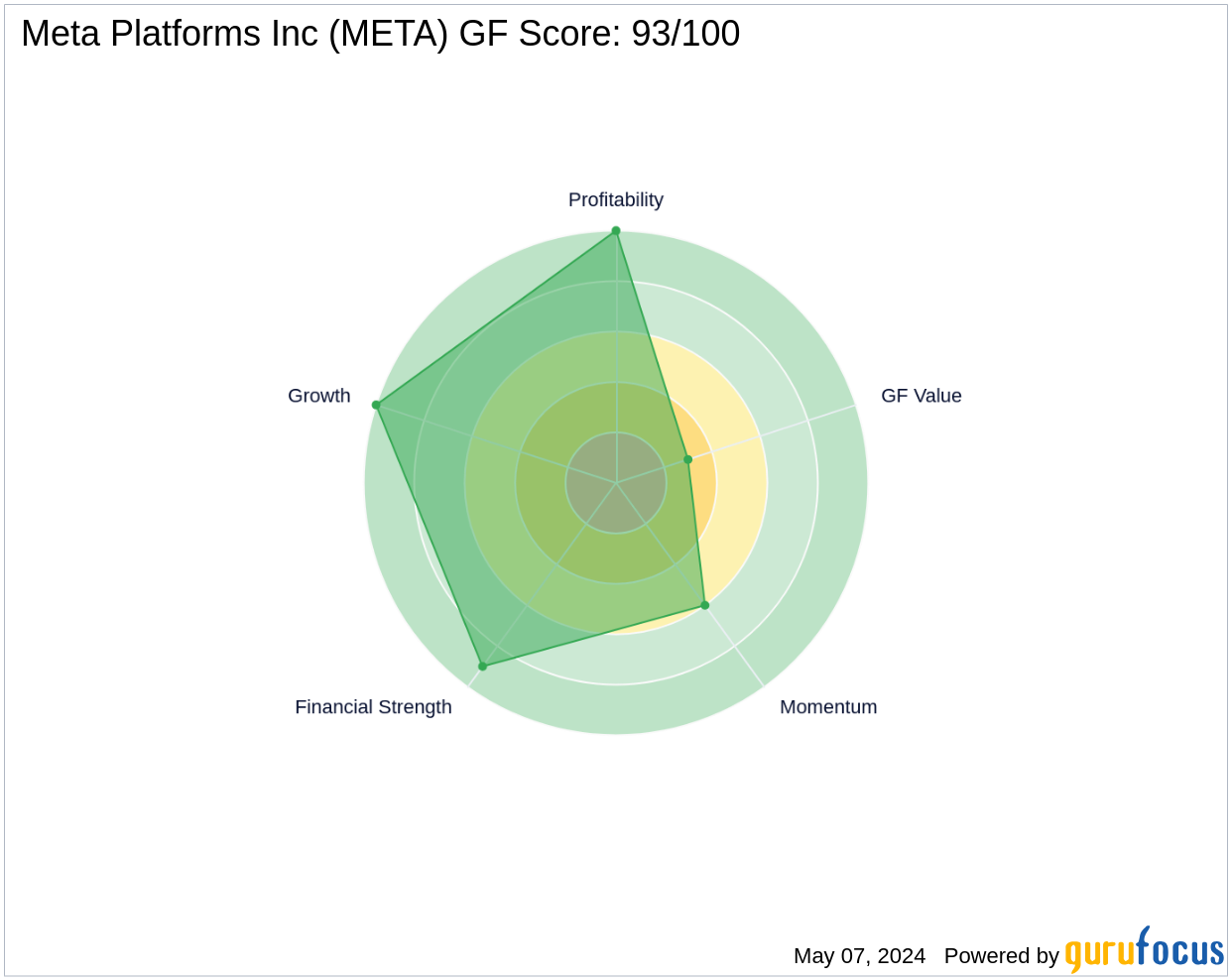

Stock Split Prospects Abound in Meta Platforms and CrowdStrike

The world of investment often shines a spotlight on stock splits, not just because they bring down the per-share price, but also because they serve as indicators of future returns rivalling the market. Historically speaking, the stocks that split have managed to perform 13% better than the S&P 500, a year post their split announcement. In the recent three years, Meta Platforms and CrowdStrike have yielded impressive returns, 255% and 185% respectively.

Both these companies are now potential candidates for stock split, courtesy the substantial price appreciation. As per certain market analysts and investment pundits, both these stocks represent sound investment options as of today. Meta Platforms boasts ownership of four among the top seven social networking platforms, a strategic advantage that essentially enables them to source extensive consumer insights.

Their capability to facilitate targeted advertising campaigns for distinct brands has positioned them as the second-largest adtech firm across the globe. eMarketer predicts a steady growth in Meta’s share of this market continuing up until 2026. Further cementing their financial position, the first quarter results revealed robust figures, surpassing projections across all major areas.

Their revenue witnessed a 16% surge, reaching $42.3 billion, while their operating margin demonstrated a 3% expansion. The GAAP net income, per diluted share, experienced a 37% growth, amounting to $6.43. Their future aspirations involve integrating artificial intelligence (AI) into the entire ad creation process by 2026.

As per a recent exploration, a brand could offer a product image it wishes to propagate, outline a budget, and have AI take care of the entire ad – beginning from imagery, video, to text. This forward-thinking innovation positions Meta at the forefront of the burgeoning adtech market, which is expected to witness an annual growth rate of 14% up until 2030.

This growth prompts a prediction among Wall Street insiders for Meta’s earnings to experience an 18% annual hike over the forthcoming three years. With such promising prospects, the current earnings multiple of 27 times seems like a reasonable valuation. Hence, those taking the long-view in investments should confidently consider buying a stake in this stock today.

CrowdStrike, best known for its leadership in endpoint protection to ensure device safety (servers, desktops, laptops, et cetera), operates in the cybersecurity industry. The recently released first-quarter financial report of CrowdStrike has yielded a mixed bag of results. On one hand, bolstered by high retention rates, revenue saw a 20% increase, amounting to $1.1 billion.

On the other hand, they observed an 8% drop in non-GAAP net income per diluted share, coming down to $0.73, as a result of an injection of funds aimed at augmenting go-to-market abilities and automation. Going forward, several growth catalysts are aligned in favor of CrowdStrike. Identified as the industry leader in managed detection and response – a service which allows companies to offload their cybersecurity requirements to skilled professionals, the company should capitalize on the ongoing severe labor shortage within the sector.

All things considered, the company estimates that its addressable market could reach a staggering $250 billion by 2029. Unfortunately, the existing valuation seems overpriced at 124 times the earnings. While it’s true that CrowdStrike has consistently outperformed consensus estimates by approximately 12% in recent six quarters, but the stock would still be pricey even if this trend carries forward.

From a personal perspective, it would be more prudent for investors to add CrowdStrike to their watchlists instead of pursuing it at its current price. Potentially, the company carries the promise of becoming significantly more valuable in the times ahead. However, the present inflated valuation might provide purchase opportunities during market downsides in the near future, particularly in view of the prevailing macroeconomic instability.