Unveiling the Strengths of Value-Oriented Companies

Value-oriented companies are often characterized by their comparatively low valuations with respect to key fundamentals such as revenue streams, dividend returns, net cash flow, and growth rate derived from both the business and wider market trends. These characteristics are often manifest in their lower share price relative to the company’s intrinsic value, fostering investor anticipation that these value stocks will outstrip overall market growth. The group encompasses some of the largest and most acclaimed companies globally such as Berkshire Hathaway, Johnson & Johnson, and Procter & Gamble, making them worthwhile investment pursuits. Represented globally by the Vanguard Value ETF (VTV), these value-sector stocks have consistently outshined the broader market, offering a return of 32.19% over the past year which exceeds the S&P 500’s total returns of 31.27%.

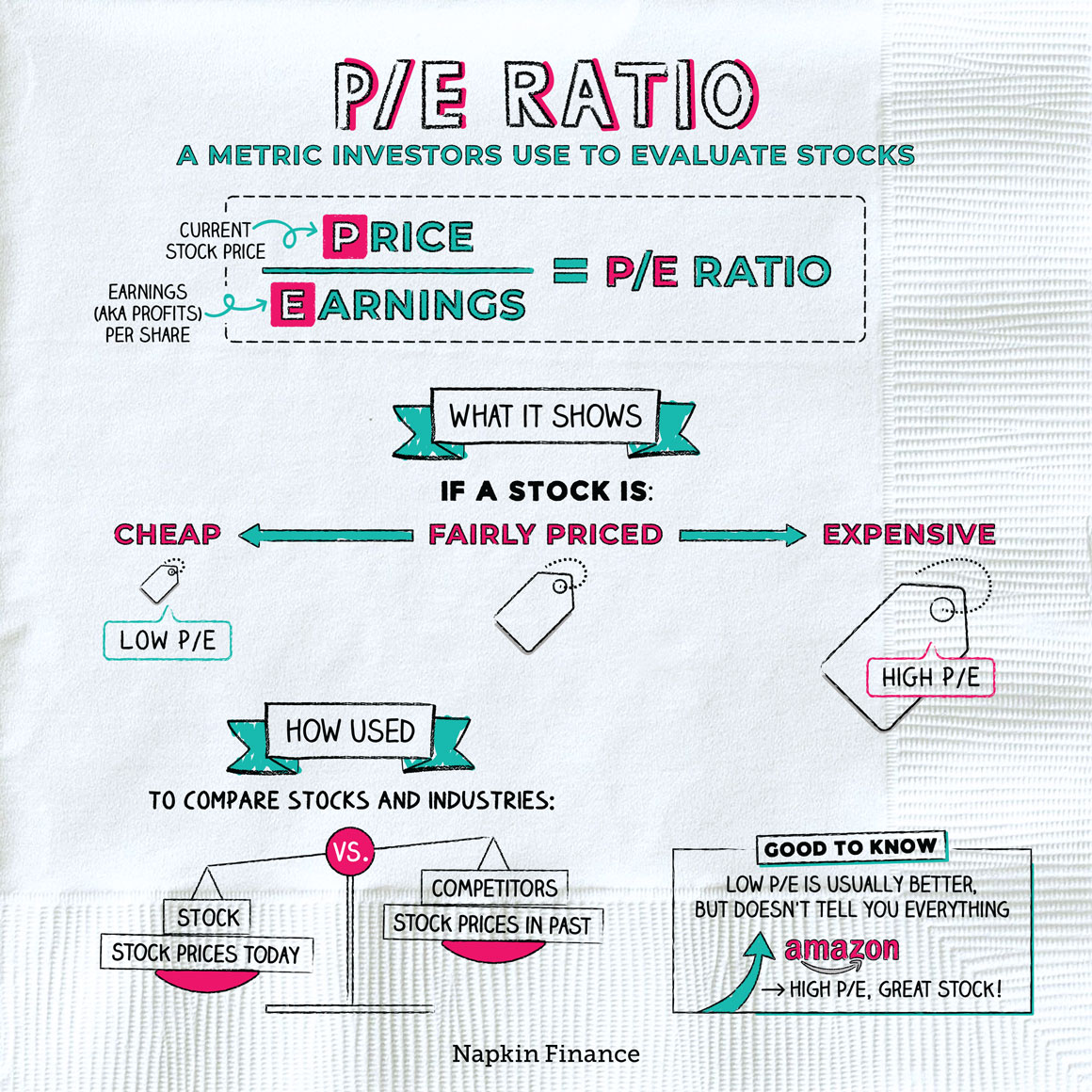

Consider the week of October 25, 2021, value stocks across many sectors emerged as top performers, largely owing to inflation fears and supply chain interruptions that deflated valuations of diverse companies. When scouting for enviable value stocks, investors consider a myriad of attributes key among them being a low Price-to-Earnings ratio. This is a prevalent measure of stock valuation, juxtaposing the stock’s value against its earnings. The P/E ratio is derived by dividing the share price by the earnings per share which value investors seek to be 15 or lower, contingent on comparisons within the respective market sector and industry.

As of June 15, 2021, the average P/E ratio of the S&P 500 stood at 45.11. Another pivotal metric to keep on the radar when seeking value stocks is a Reasonable Price-to-Book Ratio. It computes the market value against the company’s book value, comprised of total assets (whether tangible or intangible) less total liabilities. P/B ratios below 1 are often deemed commendable as they imply market value is inferior to the book value; Nevertheless, P/B ratios are not without their limit, and are typically appraised in conjunction with the Return on Equity (ROE). Generally, an ROE close to or above 15% is deemed acceptable.

No business is spared from the perils of excessive debt, irrespective of how stellar it may appear on the surface; High debt levels can precipitate the downfall of even industry behemoths. The Debt-to-Equity (D/E) ratio, therefore, becomes a pertinent gauge of a company’s financial leverage. For the prudent value investor, a figure beneath 2.0, and ideally without leverage (less than 1) is desirable. Furthermore, a preference is harbored for well-covered dividends. Rather than speculating, a value investor typically seeks a long-term share in the company’s profits, symbolized by regular dividends.

For these dividends to be meaningful, they must be sustainable, underscored by the fact that numerous companies scaled back or entirely omitted their dividends during the last market slump amidst unrealistic expectations and the potential to unnerve investors. As a rule of thumb, a dividend payout ratio below 50% is considered healthy, although in stable sectors such as consumer goods and utilities, this figure could rise to as much as 75%.

Value investing’s virtue lies in its ability to generate significant wealth over time. However, it requires a blend of several key traits, paramount among them patience, discipline, and a logical mindset. In the words of Charlie Munger, ‘A few major opportunities, clearly recognizable as such, will usually come to one who continuously searches and waits, with a curious mind, loving diagnosis involving multiple variables.’ This approach, combined with the aforementioned fundamentals, can potentially lead to success in the field of value investing.